"Even after last week’s 2.5 percent rally, Russian equities have the cheapest valuations among 21 emerging economies tracked by Bloomberg. The Micex Index’s 12-month estimated price-to-earnings ratio was at 4.3 today, compared with a multiple of 10.7 for the MSCI Emerging Markets Index."

Berg September 23rd

Now there are many good reasons for Russia to trade at a discount to developed markets - see here for an incredible exchange between Russian management and a fund manager working at an overseas shop. Russian demographics are also horrible (and people complain about Japan!), corporate governance is non-existent, the state is run by thugs, they hate paying out dividends and the oil companies are going into slow run-off mode.

But 4.9x times earnings? That's cheaper than Pakistan (8.0x earnings - Pakistan is actually trading at a premium to it's five-year average!) and on par with where Korea traded at during the Asian Financial Crisis. Things may be crappy in Russia but they are not 4.9x earnings miserable, and Russia is far less of a failed state than Pakistan. Moreover, unlike Pakistan going into Lehman (or even now), or Korea going into the Asian Crisis, Russia runs a current account surplus. As discussed in the previous post, Russia is about 30% below it's five-year average book value, its currency looks cheap (see here for one view on why Russia would let its currency appreciate, I am not sure I totally buy the rationale but there is a logic to it) and the country is just very cheap on about every metric.

Source: Credit Suisse

Source: Credit Suisse

The OS was also intrigued to hear on a podcast with Mebane Faber (go to around 28 minutes 30 seconds in - skip the first 20 minutes of drivel, and focus on the interview. Some smart points made by Meb and actually the interviewer from time-to-time) that Russian energy companies were among the cheapest sub-segments globally in the equity universe - on par with Greece! Jim Grant was also on CNBC a month and half back fielding the usual repertoire of silly questions from the interviewers, but he touched on the issue of he Russian oil plays.

The OS was also intrigued to hear on a podcast with Mebane Faber (go to around 28 minutes 30 seconds in - skip the first 20 minutes of drivel, and focus on the interview. Some smart points made by Meb and actually the interviewer from time-to-time) that Russian energy companies were among the cheapest sub-segments globally in the equity universe - on par with Greece! Jim Grant was also on CNBC a month and half back fielding the usual repertoire of silly questions from the interviewers, but he touched on the issue of he Russian oil plays.

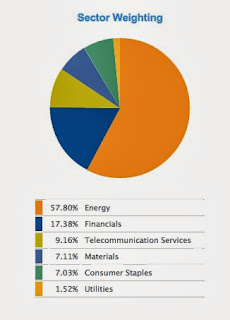

Reflecting upon this then, it shouldn't be too surprising then that the Russian market itself is dirt cheap as the MSCI Russia index is very commodity-heavy at 64% (basically, energy); then banks at 17% and telcos at 9%.

However, given the lack of Russian language skills (the Oriental Speculator studied - if it could be called that - Russian for one year at high school and was frankly horrible at it) and a detailed understanding of the politico-economic dynamics in Mr. Putin's playground, the Oriental Speculator is a little wary of going for single name picks and is leaning towards the funds route.

So far, the attention of the OS has been focused on the ETF channel and the MSCI Russia Capped Index ETF options. The MSCI Russia Capped Index is basically the same as the MSCI Russia Index except MSCI try to prevent any one stock becoming disproportionately overweighted in the index make-up. Which in Russia's case is probably quite sensible as Gazprom alone is 23% of the index and Sberbank is 14% (basically, Sberbank IS the financials sector in Russia).

For the MSCI Capped at construction and at each rebalancing, if the weight of the largest company in the sister MSCI Russia Index is greater than 30%, its weight in the MSCI Capped gets stopped out at 30%. The weight of the remaining Group Entities are then increased in proportion to their weight prior to such capping. The remaining stocks are capped at no more than 20% weighting and so on. So basically, the two largest names in theory will never exceed 50% of the index. Further deats here.

There are, at least, two ETFs out there doing this index:

1. ishares MSCI Russia Capped (ERUS)

2. db x-trackers MSCI Russia Capped Index ETF (3027.HK)

The Oriental Speculator has after decided the db option is probably the more favorable of the two given it trades in HK and thus does not get hit by capital gains. As far as the OS is aware, this is the only Russian ETF listed in HK (HKEX has a list of the ETFs that trade on the exchange available here.)

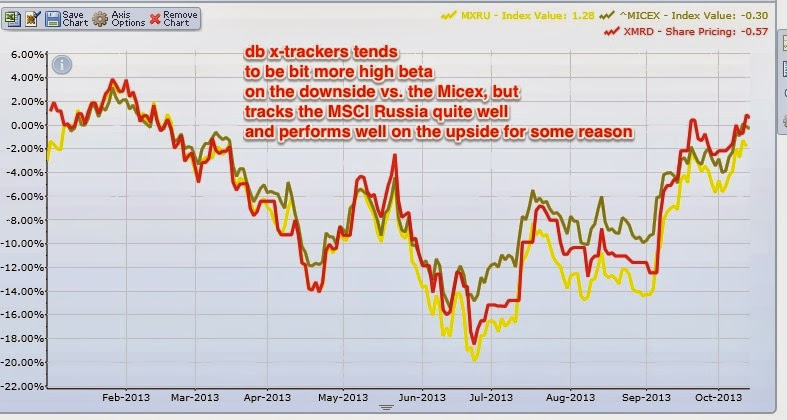

Within the framework of the capped index, the db ETF tweaks things a little further, and caps an individual company's weight to 25% and quarterly at 20%. That actually means at present the capped index and db's etf is exactly the same as the normal MSCI Russia index, which itself is basically very similar to the MICEX index (albeit, it appears to be a bit higher beta).

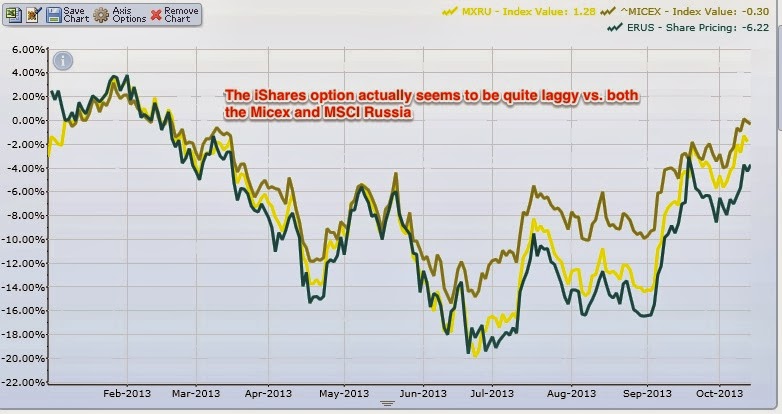

iShares takes a slightly different tack as it then uses a 25/50 strategy on the capped index:

"The MSCI 25/50 Indices take into account the investment limits required of regulated investment companies, or RICs, under the current US Internal Revenue Code. One requirement of a RIC is that at the end of each quarter of its tax year no more than 25% of the value of the RIC's assets may be invested in a single issuer and the sum of the weights of all issuers representing more than 5% of the fund should not exceed 50% of the fund’s total assets."

This - the Oriental Speculator presumes - gives rise to the slightly different constituent weights for the ETFs and thus valuations. For while the 25% rule doesn't appear to be breached in the iShares case, the sum weight of all 5% constituents breaching the 50% mark does appear to be.

Now, the OS is not sure how iShares actually compute the weightings for the stocks over 5% in the actual underlying, but given the capped index is already messing with the original index then iShares is layering in more voodoo on top; and the OS is not a US citizen so doesn't care about the RIC code, the OS doesn't see the iShares as having a compelling selling point over DB's etf in the composition field. (That having said, OVERALL sector weightings are similar for both, it's just what they've chucked in there to get the weightings is different.)

Source: iShares

Source: Deutsche

An obvious problem though is that the iShares ETF is also SUBSTANTIALLY more expensive than the index - although this is probably be due to iShares favoring growthier shares in its rebalance. Now the below data points are from August 30th but the market has rallied since then so I am guessing the iShares ETF is probably MORE expensive than it was back in late August. (Note also the MSCI Russia is not quite the MICEX but tracks it pretty well, albeit it seems to fall more on the down-legs than the MICEX.)

Source: Deutsche

Source: iShares

Meanwhile the db ETF/capped index's PE went for 5.1x back on August 30th. So you're getting cheaper and more faithful exposure to the Ruskies via ze Germans.

Now the one issue that could be a wrinkle, is the db option is a synthetic etf. What is a synthetic etf I hear you ask? Some deats on these here. The issue with synthetics is that you are generating your returns via a swap agreement, and thus are exposed to counter-party risk.

However, there have been a number of improvements in ensuring that investors are protected from the counter-party blowing up. The principal form being a funded swap model and the Russian Capped appears to be one of these - see page 24 of this Morningstar document. So the OS suspects that this is actually not a huge concern and DB is generally considered too big to fail (although one wonders if things get really sticky would Fraulein Merkel care that much about saving overseas investors in a Russian ETF... probably not).

Thus, out of the ETF names the OS can find that allow one to play Russia, the HK ETF is probably the better option: no CGT, and it represents a more faithful and cheaper way to play in Mr. Putin's playground (assuming one is comfortable with big exposure to commods and banking). Still the OS is gonna take a poke around to see if there are any closed end funds out there trading at interesting discounts.

No comments:

Post a Comment